Article Info

Expropriation is Not Competition, Even in France

The Wall Street Journal published an article on CLEC activity in France which praised the efforts of the French equivalent of UNE regulation and highlights the ‘competitive’ environment it has created. Yesterday the WSJ covered (and we commented on) the German government and Deutsche Telekoms efforts to have UNE rolled back.

UNE, like Net Neutrality, is a confiscatory government policy that expropriates an asset from it’s owner.

The article focuses on the ‘success’ of a French CLEC called Iliad.

One telecom company in particular has exploited the changes and created competition in France — a start-up called Iliad. Over 1.1 million French subscribers pay as low as €29.99 ($36) monthly for a “triple play” package called Free that includes 81 TV channels, unlimited phone calls within France and to 14 countries, and high-speed Internet. The least expensive comparable package from most cable and phone operators in the U.S. is more than $90, although more TV channels are generally included.

And this is how Ilaid’s model works, for those who need a quick into to what UNE regulations are all about.

France Telecom had to allow alternative providers like Iliad, Neuf-Cegetel, and Telecom Italia SpA’s Alice to install their own equipment in the massive underground centers that collect thousands of phone lines. Regulators determine how much France Telecom could charge providers to rent its lines and how many days France Telecom has to fix service problems reported by competitors’ customers.

The reality? The fantastic broadband performance figures Iliad delivers are from a subset of users that happen to be close to central offices. Using UNE, Iliad can decide which customers they can market to, claim those lines from the incumbent telco, and then leave the high cost/low margin business to the incumbent.

CLECs like Iliad are only as good as the infrastructure they can free ride on.

The same situation existed in the USA until the Brand X decision was handed down, and that led to the rapid unraveling (2003, 2004, 2005) of domestic UNE regulations. The result? AT&T (T ) and Verizon (VZ) have now committed billions of dollars to build state of the art infrastructure.

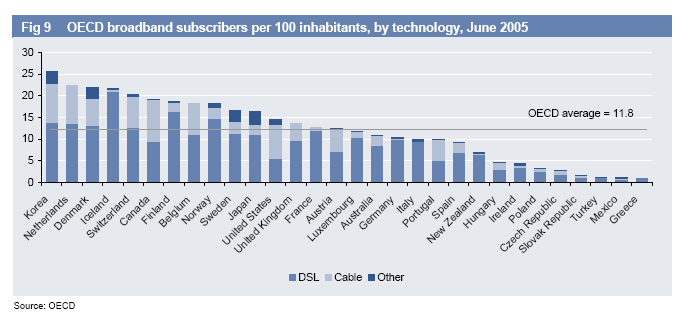

The fact is broadband penetration in France and Germany is less than the USA, and real deployment of advanced FTTH infrastructure is nil in Europe with the exception of muni fiber in Amsterdam.

The fact is broadband penetration in France and Germany is less than the USA, and real deployment of advanced FTTH infrastructure is nil in Europe with the exception of muni fiber in Amsterdam.

The real result of the ‘success’ of Iliad and other CLECs is France Telecom isn’t deploying any new advanced infrastructure because they don’t want to be forced to hand it over to a CLEC. Deutsche Telekom, France Telecom, and Telefonica are all refusing to build new infrastructure until the obligation to allow another to free-ride on top of it is removed. This has pitted them against the wishes of the EU- which was the focus of my post yesterday.

Companies only invest risk capital when the potential returns warrant it, regardless of the wishes and magical wand waving of pundits and politicos in Brussels or Washington DC. Telcos will simply refuse to make new investments in technology if the upside rate of return is regulated by a government entity and the downside risk is left unlimited.

The only solution is to create an environment where multiple providers are financially incentivized to build competitive access infrastructures.

Here’s a summary of the blogosphere. Not surprising, everyone confuses expropriation with competition.

Hum, I would say that your position is ‘very’ special.

”

UNE, like Net Neutrality, is a confiscatory policy that expropriates an asset from it’s owner.

”

I should review my economy fundamentals about the limit of the free market when dealing with non-replicable infrastructure assets !

Anyway, very interesting blog!

:-)

Andrew

Again, I like to go to the empirical data rather than the political argument. After Free started taking customers, France Telecom responded by dramatically increasing broadband investment, including ADSL2+ to 95% of the country. That’s far ahead of anywhere else in the world. A long dormant VDSL plan has been revived after some neighborhoods in Paris started being served by a new fiber builder.

Everything I know suggests competition (even the semi-artificial unbundling) is far more likely to get a telco investing than “incentives”, including de-regulation. The most dramatic case in here in the U.S. After UNE-P was thrown out, SBC in 2003 essentially stopped broadband deployment, which has been stuck at 76-77% for three years.

The investor in you, rather than the politician, should recognize that as a case of a company cutting capex to prop up short term results, rarely a strategy that pays off. SBC capex is currently only 70% of depreciation.

That we’re doing so after some of the most extreme deregulation in the world is the political lesson I choose to draw. I also note SBC’s poor financial results ongoing.

db