Article Info

Das Steigende Telekom (The Rising Telekom)

The WSJ Heard on the Street column ($$$ link) looks at Deutsche Telekom’s (DT) valuation. I’ve included a good summary of the metrics at the end of this post for those who don’t have access to the online WSJ – courtesy of Seeking Alpha’s Telecom Stock Blog.

The WSJ Heard on the Street column ($$$ link) looks at Deutsche Telekom’s (DT) valuation. I’ve included a good summary of the metrics at the end of this post for those who don’t have access to the online WSJ – courtesy of Seeking Alpha’s Telecom Stock Blog.

The WSJ article makes the case that even though the valuation of Telekom is attractive on paper, the continued price erosion in wireless and expanding competition in broadband will cap revenue growth.

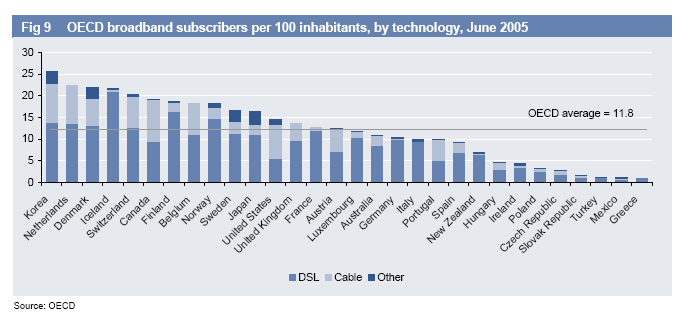

What the article misses is the groundswell in Europe to deregulate the Telecom sector further in order to spur deployment of next generation broadband infrastructure. Regardless of what the Digital Elite want you to believe, the US is ahead of France, Germany, Spain, Italy and the UK in broadband deployment. And the gap in next generation services is growing. From the article:

In a bid to separate itself from the pack, Deutsche Telekom is spending €3 billion ($3.64 billion) to build a broadband network that will connect residential customers to the Internet at a much faster speed than is currently available and allow it to offer a “triple play” of high-definition television, wireless and Internet access. But regulators in Brussels want to force the company to share the network with rivals at imposed rates, and high-definition TV is expected to remain a marginal business in the near term.

Spanish and French carriers are agitating with the EU to remove the requirement to share the network (UNE) on the basis that it will stifle new broadband infrastructure deployment – I think they are right and that they will get their way. The German Government is throwing it’s weight around the EU and the last thing the Europeans want to do is fall further behind the US in broadband deployment.

Expect to see Deutsche Telekom secure more, not less market share once this happens, and expect higher, not lower margins when it does. People will get advanced broadband, but they will have to pay for it. Es gibt kein freies Mittagessen.

Take this trend, and combine it with the competitive advantages of a carrier offering both fixed and mobile services and Telekom has distinct advantages, not disadvantages over it’s rivals. Softbank bought Vodafone’s mobile business in Japan for this exact reason, and I think it’s a winning strategy. Check out my thoughts on the acquisition.

From Seeking Alpha:

- Share Price: DT shares have dropped 10% over the last year on the background of general telco weakness in Europe and falling revenues from fixed-line services. Its dividend yield, therefore, is 5% higher than peers Vodafone (VOD) and Telefonica (TEF)

- Enterprise Value/EBITDA: EV is 5.4X EBITDA, compared with 5.8X for European telcos (Goldman Sachs estimates). Juan Carlos Acitores from Spanish firm Ahorro Corporación Financiera SV has higher earnings estimates for DT resulting in a 4.8 EV/EBITDA multiple, one of the lowest in global telecom.

- P/E: DT is currently trading at 12X expected 2006 earnings, slightly higher than competitors’ P/E. According to Acitores, who has a ’strong buy’ recommendation on DT, “The stock is significantly undervalued.â€

- Falling Operating Earnings: Thomson Financial reports that earnings per share are projected by analysts to be €1.14 in 2006 and €1.21 in 2007 (2005 earnings were €1.31 per share). Analysts expect Vodafone and AT&T, on the other hand, to grow earnings by more than 9% in 2006 and 2007.

- Falling Revenues: DT’s domestic revenue-the source of more than half total revenue-dropped 1.6% in 2005. Wireless prices are expected to fall up to 20% this year, and the company has lost substantial market share in DSL (from 83% in 2004 to 62% in 2005).

- Tough Restructuring: DT slashed net debt from €74 billion in mid-2001 to €38.6 billion. The current restructuring plan calls for eliminating 32,000 jobs over three years at a cost of €3.3 billion. And according to the WSJ, “some analysts say that even the 32,000 job cuts wouldn’t be enough to get operations sufficiently lean.â€

- T-Mobile USA: With a 27% increase in revenue last year, DT’s US mobile offering provides a glimmer of light. However T-Mobile’s ARPU has been declining faster than rivals’, and churn has been a bigger issue as well. “Because T-Mobile doesn’t have the same amount of spectrum as its competitors, it can’t offer expensive third-generation services to its customers. The unit will have to spend several billion dollars in the next couple of years to upgrade its network.â€

{kind=link}

This is a huge issue for European telcos. If the incumbents get their way on fiber, then the unbundlers’ investments in copper are effectively stranded, and Iliad et al are in a world of trouble.