Great stuff today over at the Global Crossing (GLBC) blog, where they spill the beans on their internal investigation into the cost/bit for Ethernet vs. SONET/SDH router interfaces.

The conclusion? The biggest price disparity isn’t necessarily Ethernet vs. SONET interfaces. It’s the difference between big iron routers from vendors like Cisco (CSCO) and scaled up switch routers like the Cisco 7600 or Cat 6k or equivalent products from Force 10.

Continue reading ‘Dirty Secrets of Router Interface Pricing’

England is near the top of the list of countries I don’t like to visit. My wife likes watching the tedious Victorian England dramas of BBC “Masterpiece Theatre”. I last about 10 minutes until their images force memories of stuffy rooms, bad heating, weird ergonomics and truly god-awful food to resurface.

England is near the top of the list of countries I don’t like to visit. My wife likes watching the tedious Victorian England dramas of BBC “Masterpiece Theatre”. I last about 10 minutes until their images force memories of stuffy rooms, bad heating, weird ergonomics and truly god-awful food to resurface.

There is one exception to my stereotype. British Telecom’s (BT) 21st Century (21CN) initiative. No Victorian Bric-a-Brac here.

Continue reading ‘BT’s 21CN - Reversing a Victorian Tradition’

Infinera filed an S-1 today, the link is here.

First impressions? I’m not surprised that the company isn’t generating an operating profit. But I am a bit shocked that their cost of goods sold is higher than their revenue. I need to spend more than 5 minutes looking at the S-1 but this one fact jumped out immediately.

Here’s a quick statistic worth sharing. Cisco (CSCO) CEO John Chambers spoke yesterday at the Credit Suisse Tech Conference and made the following point.

Cisco’s market capitalization has increased from $10B in January 1995 to $110B in November 2005 to $165B in November 2006; during that same period, the aggregate market capitalization of its 12 largest competitors has declined from $71B to $62B to $55B.

Wow. I’d like to get the detail behind this one.

Full Disclosure - I hold Cisco puts as a hedge against other positions. Lucky for me they are not positions in Cisco competitors…

It’s not just a catchy title. I lost my FiOS connectivity Saturday morning, rendering my Verizon tripe-play package of voice, data, and television inoperative. The culprit? Squirrels. Continue reading ‘Squirrels Ate My FiOS’

I know two American engineers who have relocated to China to lead optical module design teams at Chinese equipment companies. They live and work in China for Chinese companies, using their skills to build custom modules - skills no longer in demand from their American Tier-1 telecom equipment employers.

I know two American engineers who have relocated to China to lead optical module design teams at Chinese equipment companies. They live and work in China for Chinese companies, using their skills to build custom modules - skills no longer in demand from their American Tier-1 telecom equipment employers.

Continue reading ‘Dr. Strangelove, Or: How I Learned To Stop Worrying and Love Huawei.’

The big deal isn’t the iPhone itself, which is what the mainstream investment, gadget and tech media is focusing on. It’s the way that it will fundamentally challenge how carriers have coupled services with connectivity with a hardware distribution monopoly.

Continue reading ‘What Matters About The Apple iPhone’

Wading through my morning reading I happened upon an Acme Packet (APKT) white paper that did a good job explaining my apprehension about Akamai (AKAM) and how their business might be commoditized. In the long term, do SIP and managed media sessions replace the media caching model?

Continue reading ‘SIPlified Content Distribution’

Cisco swallowed another chip company this morning, Greenfield Networks. The notable thing about this acquisition is that Cisco rival Huawei/3Com built their high end system around the Greenfield device. I’m willing to bet that Greenfield was a lot more important to Huawei/3Com than it was to Cisco. And I’m willing to bet that’s why Cisco bought them.

Continue reading ‘Cisco’s Scorched Earth Strategy’

NPU companies consistently make the case the market is moving into their domain and that technology is their edge, right up to the point they go out of business.

NPU companies consistently make the case the market is moving into their domain and that technology is their edge, right up to the point they go out of business.

Continue reading ‘EZ-Chip and Raza Micro at Gilder Telecosm 2006′

Infinera took the bold and stunning risk of angering the Gilder priesthood by illustrating that an all optical network was not the future and not the best solution.

Continue reading ‘Death of the All Optical Network - Gilder Telecosm 2006′

This was a very interesting debate among some very heavy hitters who operate data centers about where the bottlenecks are in the data centers, and if the new model of massively distributed computing in one centralized data center is a sustainable model.

Continue reading ‘Storewidth Bottlenecks - Gilder Telecosm 2006′

Anyone know where the next ten-bagger investment is in the Telecom sector? Does anyone believe such an idea is even possible anymore?

Anyone know where the next ten-bagger investment is in the Telecom sector? Does anyone believe such an idea is even possible anymore?

Continue reading ‘The End of Telecom As We Know It And I Feel Fine’

FSAN has completed their first GPON interoperability testing. Interoperability of GPON systems is important, since the ITU standard ultimately should yield systems that interface more smoothly than the loosely defined GE-PON specification.

FSAN has completed their first GPON interoperability testing. Interoperability of GPON systems is important, since the ITU standard ultimately should yield systems that interface more smoothly than the loosely defined GE-PON specification.

Continue reading ‘GPON Interoperability Smokescreen’

How Cisco built a billion dollar business built on the backs of their optical module suppliers, and how this business has fueled the majority of their earnings growth.

Continue reading ‘Cisco’s Optical Illusion’

OK, since I’ve been called out by Om Malik, I’m going to let rip with a stream-of-conciousness monologue on optical. No backspace key, no delete key, spelling corrections ex-post-facto. Here goes.

Continue reading ‘What’s Going On in Optical’

Steve Jobs is speaking today. The world breathlessly awaits. The photo illustrates that his goal of global domination draws closer.

I think the second wildest fantasy of any marketing guy is to wield the power that Steve Jobs holds.

Continue reading ‘The Master of the Tech Universe is Speaking’

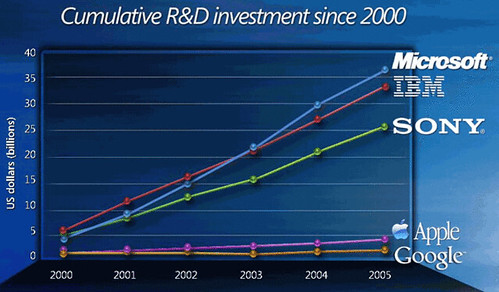

Paul Kedrosky highlights one slide presented by Craig Mundie at Microsoft Analyst Day that compares the cumulative R&D investment of Microsoft (MSFT) and Google (GOOG), among others.

Two ways to look at this.

- Google, Apple (AAPL), while highfliers, cannot have possibly built an insurmountable competitive advantage because of the relatively low investment they have made. Microsoft has huge latent value as the result of accumulated R&D spending. The asymmetry in the ability of these companies to invest is not appreciated.

- Microsoft has an exceptionally poor return on R&D when compared to peer companies and this slide illustrates that point perfectly. Microsoft’s decision to spend even MORE on R&D is the WRONG decision since they have not figured out how to spend R&D efficiently

This slide really amplifies market concerns that Microsoft’s plans to increase R&D are misguided. I didn’t hear Mundie speak, and the slide is out of context, but I don’t think it makes the argument investors want to hear.

Three Japanese Carriers were sunk by a handful of American fighters in the Battle of Midway and turned the tide of the Pacific war. The World Trade Center was destroyed by a handful of thugs.

Russia also repelled the Germans in 1944 by taking 20 million casualties.

Which way to go? I suppose you only pick the latter when you don’t know how to do the former. The market, or at least the market we are in now, rewards tactical brilliance more than human wave tactics.

From Telephony Online:

In a research note issued this morning, UBS analyst Nikos Theodosopoulos said Verizon (VZ) is likely to pick Alcatel (ALA), Motorola (MOT) and Tellabs (TLAB) as its GPON suppliers in a twist on the carrier’s traditional dual-sourcing practices.

Typically the Bells would select two vendors, with a 70:30 deployment split between the two over the life of the contract. Who got the 70 was usually determined by technology and pricing in the early stages of the contract, establishing relative incumbency for one supplier.

Continue reading ‘Verizon GPON Selection’

Received a couple emails and a Yahoo! IM today with the same question… why no blogging?

I’m working on a detailed study on optical modules. I think I’ve found something particularly interesting.

Continue reading ‘Head Down, Working’