It’s pretty clear that the AT&T (T ) and Bellsouth (BLS) merger has turned into a proxy war over Net Neutrality, with Yahoo (YHOO) and Google (GOOG) spearheading the effort in a naked attempt to keep their distribution costs near zero. Correspondingly, Washington bloodsuckers lobbyists on both sides are gearing up.

Continue reading ‘Net Neutrality War Heating Up’

Archive for the 'Regulation' Category

I woke up in SFO at 4AM to make sure I could get to Tahoe in time for this debate. I’ve written extensively on Net Neutrality and stopped once I realized it was unresolvable.

Broadband Brawl: A Debate Over Net Neutrality

Continue reading ‘Net Neutrality Debate - Gilder Telecosm 2006′

Online Gambling was effectively outlawed in the US today. The legislation is intended to bring ‘fairness’ to the domestic gaming industry which has been harmed by the appearance of off-shore online only gaming companies. What does this mean for brick and mortar retailers squeezed by the internet?

Online Gambling was effectively outlawed in the US today. The legislation is intended to bring ‘fairness’ to the domestic gaming industry which has been harmed by the appearance of off-shore online only gaming companies. What does this mean for brick and mortar retailers squeezed by the internet?

My local town approved the FiOS TV franchise contract. I attended the first and only public hearing on the matter a month ago (and blogged it here).

Continue reading ‘Verizon FiOS TV Local Franchise Approved’

I attended a Winchester, MA town meeting tonight. The sole purpose of the meeting is to vote on cable franchise application from Verizon for FiOS TV. Meeting ran from 7:30PM to 10PM. Other than a small zoning meeting I once attended, this is my first town meeting.

I am a FiOS customer and follow FTTH issues from a financial and technical basis pretty closely.

THESE ARE RAW NOTES. I reserve right to change them if I get my hands on a transcript from the meeting.

Analysis to follow in a later post.

—————————————–

Guy from Comcast sitting next to me taking notes. Keeping tabs on the competition. Very friendly, do I detect even some sympathy for what Verizon is about to endure?

Lots of people here… they all know each other. They are all Verizon employees who live in Winchester. A little grass roots corporate push.

Board kicks off Meeting

This weekend was Town Day in the Boston suburb where I live. One of the street vendors was Verizon (VZ), who was promoting their FiOS service. Comcast (CMCSA)was there too.

This weekend was Town Day in the Boston suburb where I live. One of the street vendors was Verizon (VZ), who was promoting their FiOS service. Comcast (CMCSA)was there too.

I took the opportunity to quiz the Verizon rep on how deployment was going. The rapidity and completeness of his answers was either the result of rehearsal or intense pride.

He indicated that the surrounding towns, where FiOS TV was available, FiOS penetration was at 20%. I asked him what 20% meant and he said “One in every Five Homes”. I asked - “No tricky accounting?”. He said no, and that things were going very, very well. I asked about my town, where FiOS TV is not available and he said that penetration was about 10%, and that the lack of video impacted penetration in a big way. Towns with Video service see much higher subscriber take rates.

I was in disbelief - 20% penetration after six months of service was astounding. I pressed him for a few more minutes and he stood firm on his answers.

I then asked him when they would be getting the franchise approval in my town and he said - the Town Meeting is this Wed. Today.

Should be interesting to see what machinations are required to secure a video franchise. I’m going to go.

Looks like the WSJ managed to purchase some more computer time for their options backdating algorithm and in this mornings paper they name the new five lucky winners - click on the graphic to the right.

Looks like the WSJ managed to purchase some more computer time for their options backdating algorithm and in this mornings paper they name the new five lucky winners - click on the graphic to the right.

This issue is of interest to me since I spent over 10 years at Vitesse Semiconductor (VTSS), a company that has been roiled by this issue in the last month. It’s also one of many reasons why incentive options should always be accounted as an expense and included in pro-forma results.

Continue reading ‘Options Backdating Reloaded’

Scott McNealy, ex-CEO of Sun Microsystems (SUNW) talking about Net Neutrality (term defined) (my opinions here) in an interview with the Washington Post:

Spent today working outside in the yard wishing I was out cycling. Had a lot of time to think.

What I find funny is the same people who pound the table about how the internet was born a wild, free, medium, how this is it’s biggest advantage, and how this is the manifest destiny of the network now cry foul when the internet might evolve into paying for multiple tiers of service.

Folks who make an argument for government mandated net-neutrality are asking to halt the untethered evolution they proclaim to be essential. That’s pretty funny.

Apple Computer Inc. should have anticipated that the exclusive union of its iPod music players and online iTunes store would be challenged in France, Trade Minister Christine Lagarde said.

Anyone else find it incredibly ironic that Apple (AAPL), who lobbied tirelessly and endlessly, both domesticly and in Europe against Microsoft’s (MSFT) monopoly power, is now finding the same accusations leveled against themselves?

A copyright bill before the French parliament on downloading music and films could lead the online music store, Apple’s iTunes, to withdraw from France because it would be reluctant to opening up its proprietary system, experts say.

Apple Computer Inc. has always refused to allow its paid-for music files downloaded via iTunes to be converted into another format, which would allow them to be listened to on a music player other than its iPod.

We’re not Apple investors. I don’t own an iPod because I refuse to buy into the ‘roach-motel’ model of iTunes, where any music purchased is locked up in the iTunes universe ad infinitum. But I admire how Steve Jobs cleverly used sexy hardware and ease-of-use to convince millions of consumers to lock themselves into the Apple DRM model.

I love the hardware too, and if they had a subscription model I would jump. I think the only reason Apple has not offered a subscription model is that they want consumers to buy songs on iTunes in order to landlock them as Apple customers, eventually migrating them into other areas like Video and the digital living room. Nice Job Mr. Steve.

Now, having obtained near market share dominance of 80%, his Steveness has now encountered the same antitrust forces he helped unleash years ago in his battles with Microsoft.

(Minister Christine Lagarde) met with Charles Phillips of Oracle Corp., John Chambers of Cisco Systems, and Scott McNealy of Sun Microsystems, but not with any Apple Computer Inc. representatives.

McNealy. Oracle. Sound familiar? This was the same wrecking crew that went after Microsoft.

Comme on faict son lict, on le treuve.

Translation: “You’ve made your bed, now lie in it”. It is of 16th century French origin.

How appropriate.

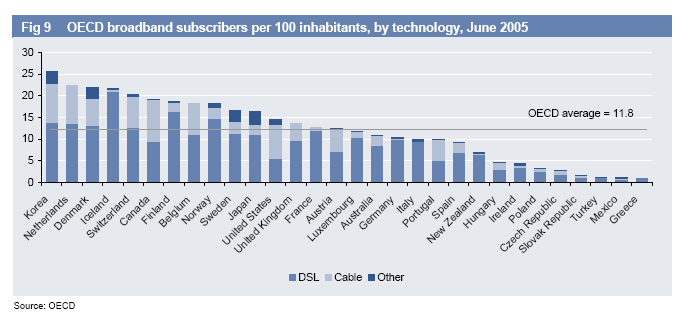

The OECD released updated broadband statistics yesterday. The US is ranked 12th. Included is some historical trend data that I think sheds some light on why a broadband ‘gap’ exists between the US and the rest of the world.

I don’t believe the broadband gap is a problem that needs to be solved. I think many folks are happy with dial-up in the US, and don’t subscribe to broadband because no incentive exists for them to switch.

In Europe, few people were happy with dial up. Unlike the USA, where local phone calls to the AOL modem pool were free, Europeans were charged per-minute fees. There was no such thing as a free local call. Europeans who spent hours on the phone with their ISP hated dial up not just for poor speeds but also high cost. This leads to a large proliferation of Internet cafes and initially, low internet use.

Let’s look at growth trends in Asia, North America, and the EU over the last few years.

Note - The EU-15 are comprised of Belgium, France, Germany, Italy, Luxembourg, The Netherlands, Denmark, Ireland, United Kingdom, Greece, Portugal, Spain, Austria, Finland, Sweden.

I think there is a pretty simple explanation at work here. Once broadband technology became available, Europeans rapidly ditched their dial up lines not just because of speed, but because of cost. European broadband exploded with a spectacular 73% CAGR while the USA grew at a slightly less rate of 39%. I don’t think the lack of government intervention in the broadband markets provides an explanation for the difference in growth rate. The government can’t make things grow that fast and there is only one thing that can - economic substitution. There was a huge economic incentive to move to the fixed rate connections offered by DSL.

In Korea and Japan, the government creates financial incentives in other ways to move people to broadband whether they want high speeds or not.

Now that $19.99 DSL is becoming widely available in the US, and AOL has increased prices for dial-up so that they are higher than their bundled DSL offering, I expect you will see the same movement here in the US, the broadband gap with Belgium, Canada, Iceland, and Japan will be closed, and global catastrophe averted.

The Net Neutrality ship continues to sink with the recent removal of wording from legislation that would have removed the right of carriers the to tariff based on application.

I’ve always felt Net Neutrality is a concept that expropriates the property rights of carriers in order to allow media and content companies a free-ride on their infrastructure. Google, Yahoo and other media and content companies lack ownership of a layer-one digital right of way to the consumer- so the easiest approach is to legislate the theft of it.

Anyone who thinks this is a reactionary opinion should consider what Rep Ed Markey said about the failure to pass the bill. From the CNET article:

There is a fundamental choice. It’s the choice between the bottleneck designs of a…small handful of very large companies and the dreams and innovations of thousands of online companies and innovators.

What if this debate was over a privately owned road? Would Mr. Markey feel the same way?

The good of the many is more important than the good of the few. But there are laws that cover the taking of private property rights - if you determine the greater good requires that the few forfeit their deed of ownership then you should compensate them for it.

When it comes to “fundamental choice”, I’ll go with property rights over government re-appropriation any day.

Additional Observation: Note the title of the CNET article - “Republicans defeat Net neutrality proposal“. As it’s prospects wane, the debate on Net Neutrality is moving from a technical and economic argument to a political one. Never mind that 4 of the 11 Democrats on the committee voted against the provision - nothing like a little political fire-stoking to keep debate rolling.

Martin Geddes (Blog: Telepocalypse) delivered a rare dissenting opinion at the Jeff Pulver “Freedom to Connect” net-neutrality love-fest conference today. I was not there, but I can’t imagine it was a friendly audience. Earlier in the day Michael Copps, FCC Commisioner, delivered a keynote outlining the risks of net neutrality. (Note I will link to speech when text is online).

Here’s a highlight of Geddes’s speech:

An open, free net is an emergent outcome, not an a-priori input to be legislated into existence. We need to capture and accellerate the experiments in how networks are built, financed and sold; and protect those experiments from incumbent wrath until the results are in.

But most critically, don’t fossilize the network in 2006 by adopting network neutrality.

My thoughts on the subject can be found by searching for “Net Neutrality” in the search box or simply clicking here.

The left-leaning Common Cause published a good analysis of the “Astroturf” organizations supporting the telecom companies. However, the unprofessional nature of their presentation leaves something to be desired. Check out the goofy graphic at the right, and click on it to see another.

The left-leaning Common Cause published a good analysis of the “Astroturf” organizations supporting the telecom companies. However, the unprofessional nature of their presentation leaves something to be desired. Check out the goofy graphic at the right, and click on it to see another.

Astroturf refers to artificial grass roots organizations that are designed to appear independent but receive the majority of their funding from public organizations to lobby the public.

While I disagree with the arguments Common Cause makes about Net Neutrality, I don’t agree with the use of these Astroturf organizations. Some of these groups declare the fact they receive cash from Telcos and Cablecos, some don’t.

- Consumers for Cable Choice

- FreedomWorks

- Progress and Freedom Foundation

- American Legislative Exchange Council

- New Millennium Research Council

- Frontiers of Freedom

- Keep It Local NJ

- Internet Innovation Alliance

- MyWireless.org

My question is this - where does Common Cause get it’s money? I couldn’t find that anywhere on their website. Sure would be ironic if Google or other content providers were donors.

Richard Notebaert, CEO of Qwest (Q ) has a short op-ed in today’s WSJ discussing how the Net Neutrality has been twisted to serve the interests of the digital elite.

From the editorial:

According to the FCC, Net neutrality means that providers of Internet services must allow unfettered consumer access to the Internet. No one should deny or impede access to lawful sites on the Web. Everyone supports that position.

But some very big corporations are trying to redefine Net neutrality away from a focus on access, and toward something far more nebulous and self-serving. Case in point — assume an online movie provider negotiates a commercial agreement with a company like Qwest to guarantee download speeds of, say, five megabits per second, for all its customers. That’s a pretty good idea in a world where every company is trying to differentiate itself from its competitors.

“Not so fast,” cry the naysayers. They claim that the idea of a premium level of service violates Net neutrality because that online movie company’s competitors may not want to offer their customers the same benefits. Essentially, they argue that doing this would give some content providers an advantage over those that choose not to provide this service.

Well, yes it would. As an industry, we’ve always sold bigger pipes and faster service to those who wish to buy them. And yes, I suspect much of that enhanced capacity has been bought to give the purchaser an edge. That’s how a competitive marketplace works.

Once fiber and high bit rate DSL gets deployed to the curb the bottleneck will no longer be the ‘last-mile” but will be the infrastructure between the user and the supplier of media and content. Taking away the ability of carriers to use variable pricing to distribute costs according to use and demand will result in a stagnation of investment as well as higher prices for people who fund the heavy usage of others.

Notably, Notebaert isn’t a complete Telco shill, he recently indicated that the hype over peer to peer usage isn’t warranted, and isn’t impacting his network. Maybe that’s because Qwest customers have the worst DSL and broadband penetration and technology. P2P may not be as popular on Qwest’s network as it may be with others that support much higer bit rates and can deliver even-more-instant gratification.

The Wall Street Journal published an article on CLEC activity in France which praised the efforts of the French equivalent of UNE regulation and highlights the ‘competitive’ environment it has created. Yesterday the WSJ covered (and we commented on) the German government and Deutsche Telekoms efforts to have UNE rolled back.

UNE, like Net Neutrality, is a confiscatory government policy that expropriates an asset from it’s owner.

The article focuses on the ’success’ of a French CLEC called Iliad.

One telecom company in particular has exploited the changes and created competition in France — a start-up called Iliad. Over 1.1 million French subscribers pay as low as €29.99 ($36) monthly for a “triple play” package called Free that includes 81 TV channels, unlimited phone calls within France and to 14 countries, and high-speed Internet. The least expensive comparable package from most cable and phone operators in the U.S. is more than $90, although more TV channels are generally included.

And this is how Ilaid’s model works, for those who need a quick into to what UNE regulations are all about.

France Telecom had to allow alternative providers like Iliad, Neuf-Cegetel, and Telecom Italia SpA’s Alice to install their own equipment in the massive underground centers that collect thousands of phone lines. Regulators determine how much France Telecom could charge providers to rent its lines and how many days France Telecom has to fix service problems reported by competitors’ customers.

The reality? The fantastic broadband performance figures Iliad delivers are from a subset of users that happen to be close to central offices. Using UNE, Iliad can decide which customers they can market to, claim those lines from the incumbent telco, and then leave the high cost/low margin business to the incumbent.

CLECs like Iliad are only as good as the infrastructure they can free ride on.

The same situation existed in the USA until the Brand X decision was handed down, and that led to the rapid unraveling (2003, 2004, 2005) of domestic UNE regulations. The result? AT&T (T ) and Verizon (VZ) have now committed billions of dollars to build state of the art infrastructure.

The fact is broadband penetration in France and Germany is less than the USA, and real deployment of advanced FTTH infrastructure is nil in Europe with the exception of muni fiber in Amsterdam.

The fact is broadband penetration in France and Germany is less than the USA, and real deployment of advanced FTTH infrastructure is nil in Europe with the exception of muni fiber in Amsterdam.

The real result of the ’success’ of Iliad and other CLECs is France Telecom isn’t deploying any new advanced infrastructure because they don’t want to be forced to hand it over to a CLEC. Deutsche Telekom, France Telecom, and Telefonica are all refusing to build new infrastructure until the obligation to allow another to free-ride on top of it is removed. This has pitted them against the wishes of the EU- which was the focus of my post yesterday.

Companies only invest risk capital when the potential returns warrant it, regardless of the wishes and magical wand waving of pundits and politicos in Brussels or Washington DC. Telcos will simply refuse to make new investments in technology if the upside rate of return is regulated by a government entity and the downside risk is left unlimited.

The only solution is to create an environment where multiple providers are financially incentivized to build competitive access infrastructures.

Here’s a summary of the blogosphere. Not surprising, everyone confuses expropriation with competition.

The WSJ on Saturday covered efforts by Deutsche Telekom (DT) to seek deregulation of policies similar to UNE-P regulations here in the US.

The WSJ on Saturday covered efforts by Deutsche Telekom (DT) to seek deregulation of policies similar to UNE-P regulations here in the US.

Europe’s largest telecommunications company is investing €3 billion ($3.6 billion) to connect residential customers to the Internet at speeds up to 50 megabits per second — more than eight times as fast as its quickest offering so far and faster than any other connection available in German homes. The move is crucial for Deutsche Telekom’s ambitions of offering a “triple play” of services spanning telephone, Internet and television at a time when its traditional business of phone calls is being shaken by major technological upheavals.

It looks like they managed to get a copy of Verizon’s (VZ) and AT&T’s (T ) playbook…

The German incumbent is lobbying to be spared such interference, arguing that it is creating a new service and already faces mounting competition from cable, Internet and other telecom companies. It has threatened to scrap the spending plan and lay off more workers if regulators impose too many restrictions.

The German government supports the removal of UNE-P like rules and has increasingly distanced itself from regulating the telco sector. Why? Concern over a broadband gap! According to the OECD, France, Great Britain, and Germany all lag Japan, Korea, and the USA in broadband penetration, particularly in next gen technology deployments.

Another quote from the WSJ article:

The government argues that there are three steps in fostering competition: privatization, regulation and deregulation. “The third step is the one that needs the most courage,” says Joachim Wuermeling, Germany’s secretary of state for the economy. That stance, however, puts Berlin on a collision course with European Union regulators in Brussels who are responsible for setting the terms of industry competition across the Continent.

As it turns out Telefonica and France Telecom want the same deregulation, and the EU is concerned that allowing germany to deregulate would be a precedent for the entire continent. All of these carriers are making deployment of next gen broadband networks contingent on a release of obligations to lease the new infrastructure to competitive carriers.

I do not understand the mechanics behind the EU and how it represents the interests of corporations and individuals in member states, but it seems ridiculous that a sovereign country no longer has control of how a company can operate within its own borders. Who are the EU regulators looking out for? Themselves?

Companies only invest risk capital when the potential returns warrant it, regardless of the wishes and magical wand waving of pundits and politicos in Brussels or Washington DC. Telcos will simply refuse to make new investments in technology if the upside rate of return is regulated by a government entity and the downside risk is left unlimited.

I am frustrated the hypocrisy of those who lament broadband availability and technology, but at the same time refuse to allow those who make the risk capital investment to reap the benefits- instead they advocate confiscatory policies like Net Neutrality, and UNE-P.

The good news is that these debates are taking place, as we may be lucky enough to see the same destructive UNE-P legislation that was removed in the USA eradicated from three of the largest states within Continental Europe.

Thanks to Om Malik for some good data (.pdf link, in German) on German broadband policy.

Lightreading has a good quote from Scott Ford, the CEO of Alltel Corp. (AT) on Net Neutrality.

I’m here to advocate that we have grocery store neutrality. You can come to the grocery store, pay $50, and you can have just whatever you want, take a cart, just load up on it. Or Taco Bell neutrality — it’s $25 a month, I can drive up and I can have a taco or whatever, or I can come with all those people in the Verizon commercial… bring them to load up on Taco Bell.

Taco Bell neutrality, grocery store neutrality, Net neutrality… They all make the same amount of sense.

From the WSJ today($$$ link)….

Verizon (VZ), making clear its view on some implications of a confusing move by the Federal Communications Commission earlier this week, said regulators’ decision to deregulate broadband data services it provides to large business customers won’t free it from conditions imposed when it acquired MCI Inc. Verizon also said the decision won’t eliminate its obligation to continue payments to a fund that subsidizes phone services for low-income and rural customers.

It looks like access lines that were originally owned by MCI are still subject to price controls, but ones owned by Verizon are not? What about lines that were originally leased by MCI from Verizon? Anyone know a good source on the net to get good hard data on exactly what this ruling means?

What really strikes me about these recent developments is that the mainstream media could care less. When the Brand X decision was handed down, the digital elite prophesized doom at the hands of the cable and telco monopolies. The same thing happens with business broadband leased lines, you could hear crickets chirping, and good details are not readily available.

So far the only outrage is coming from Washington DC and the carriers that were previously free-riding on Verizon’s infrastructure. Here’s a quote from the best article I have found on the subject.

The latest move by the FCC is likely to face challenges from competitive carriers, say experts. But some analysts say these protests are just sour grapes, since the deregulation of business broadband is a necessary step in developing a mature, market-oriented broadband market.

“The standalone CLEC business is fading,” said Jeff Kagan, an independent telecommunications analyst based in Atlanta. “This isn’t the same industry that it was in the 1990s and the 1980s. There is much more competition. The CLECs complaining are likely the ones that haven’t evolved to change with the maturing market.”

Considering the fundamental value of these connections to businesses, two very different things could be happening:

- Businesses are aloof, and unaware of the massive monopoly that has now seized control of their key digital infrastructure

- Businesses see this as a positive development, that will give their broadband suppliers an incentive to build new, better infrastructire for them to use.

Got Facts? I’d like to get a debate started but they are in short supply.

The Telecom Act of 1996 is rapidly being dismantled. Verizon asked for, and received, regulatory relief on business leased lines provided to businesses.

Covad and Earthlink were shattered by rulings ending their right to lease back physical connections into residences. This was first challenged and won by the cable industry in the Supreme Court Brand X decision, and DSL was reclassified as an information service by the FCC shortly afterwards. At this point, the companies that own the physical infrastructure that connects your residence to the Internet do not need to share that connection with another carrier or ISP. Verizon no longer is legally obligated to lease it’s copper pairs to Covad or AOL at prices dictated by the FCC.

In December 2004, Verizon petitioned the FCC to handle business connections in the same manner. The FCC commision (two Republicans and two Democrats) voted 2-2, and the lack of any conclusion on their part automatically forced the petition to be granted. FCC Chairman Kevin Martin put his stamp of approval on the outcome yesterday.

This is very radical stuff. The MCI/Verizon merger united a company with the access lines with a company that derives it’s most profitable business from connecting businesses. A major condition of this merger was that the companies unbundle the access lines to MCI competitors- the exact regulation that was just removed by the FCC.

The ruling is likely to face significant court challenges from companies like XO communications, who provide enterprise connectivity. They are analogous to Covad in the residential market, and such a ruling is a large strategic threat to their business.

Deregulation is now driving innovation in how broadband connections are made to the home. After the FCC indicated that new investments to the home would not need to be shared, Verizon and AT&T have aggresively started deploying new infrastrucutre.

Most businesses today use 20 year old T1 or T3 technology to connect to the internet or provide intranet connectivity between their sites. Now that the carriers can set pricing on their infrastructure, and set pricing on new, more advanced infrastructure, we should see these lines finally start to be replaced.

Another observation is that a lot of duplicate last-mile infrastructure to the business will need to be built in order to navigate around the Verizon monopoly. The dark-fiber guys with connections to downtown buildings suddenly are going to have more customers like XO looking to use a new right of way.

Lot’s of thinking to still be done on this subject. It’s a very disruptive event.

UPDATE: Lightreading has a comprehensive article on this subject.